Probate is the name for the legal process of distributing assets after someone passes away. These assets can include bank accounts, real estate, vehicles, retirement accounts, life insurance, and financial investments. Before the assets can be distributed, however, they must first be gathered and used to pay creditors.

After that, the heirs can finally receive their distribution of the estate. However, even then, there are several factors that can still delay the distribution process. In our practice, it is common for probate to last about nine months. In more complex cases, probate can easily last several more months or even years. These delays ultimately mean less money and more headache for the surviving family.

Let’s go through the factors that cause delays in probate, and discuss what steps can be taken to minimize the delay.

1. Passing away without an Estate Plan

If you pass away without an estate plan, your loved ones will have to go to probate court. The court will appoint someone among them to be the “Personal Representative.” The Personal Representative will be responsible for contacting all of the financial institutions about your death. They will also be responsible for using your funds to pay creditors and ultimately make distributions to your heirs.

When there is no estate plan, the process for appointing a Personal Representative can be seriously delayed. The family will have to come to a consensus on who the Personal Representative will be before they present their choice to the court. Moreover, whoever is selected as Personal Representative is often not prepared for the role, as they had not been told to expect it. The process of going through all of your finances and contacting all of your financial institutions might be overwhelming for them, especially if they did not know your finances very well. Moreover, they will be responsible for mediating tension between the family, which is made even more difficult if members of the family do not think you explicitly wanted them to serve as Personal Representative.

Having an estate plan would minimize all of these consequences and delays. By having an estate plan, your family will already know who you want to represent your estate, which will make the process for appointing a representative much smoother. The person you select to represent your estate will also be better prepared for the role, as they are aware that they will one day need to fulfill the role.

The best way to minimize delays in probate is thus to have a clear estate plan in place, and to let your family and loved ones know about your intentions.

2. Family Tension

Even with an estate plan, family dynamics can still play a major role in probate. For example, if the only major asset that you have at the time of your death is your house, and one of your heirs would like to live in it while the other heirs would rather sell it and keep the sale value, tension will ensue and attorneys may need to get involved. All of this will ultimately lead to a delay of the probate process, and may ultimately divide the family in an irreparable way.

Feuds such as the one described happen even in the most loving of families. To avoid these feuds, it is important to not only have an estate plan, but to have one drafted by an experienced estate planning attorney. An experienced estate planning attorney will be familiar with cases such as the one described and will be able to help you think through exactly what you would want to happen if these cases occur. Your estate plan will thus be better able to help your family navigate your precise wishes for your assets, ultimately easing tension and expediting the probate process.

Hiring an estate planning attorney to draft your estate plan is one of the most important steps you can take to minimize probate delays.

3. Financial Complications

If you keep your finances private, it will be difficult for your intended heirs to know what to expect after you pass away. They may not even know where you bank and what financial investments you have. The more difficult it is for them to know your finances, the more difficult it will be for them to notify your financial institutions of your death and gather accounts.

Furthermore, if you are in debt or are not paying your taxes, your Personal Representative will be responsible for using your assets to pay your creditors and the IRS. This can cause serious delays to the probate process, especially if the Personal Representative was unaware. Creditors will ensure they receive their payments by filing claims against the estate through probate court. These claims ultimately slow down the probate process as each claim requires a hearing before a judge.

To save your family time, headache, and grief after your death, it is important that you keep your finances in order. Pay off debt when you can, and keep a clear record of it. File your yearly taxes appropriately. Let your loved ones (especially your Personal Representative) know of your finances and how to contact each financial institution in case something happens.

Even in the best of cases, probate takes a while. To minimize delays, we recommend having an experienced estate planning attorney draft your estate plan, clearly telling your loved ones of your intentions, and keeping your finances in order as much as possible. Your loved ones will already be filled with grief after your death. The best gift you can give them is preparation.

Here at Graceful Aging Legal Services, we offer software that can help our clients keep their estate in order. Contact us at 615-846-6201 or hello@galsnashville.com if interested.

Becoming an executor can be both an honor and a daunting responsibility. When a loved one names you as the executor of their will, it signifies a deep trust in your ability to manage their estate after their passing. However, the role comes with numerous tasks and legal obligations that can be overwhelming, especially during a time of grief. This guide will walk you through the steps of serving as an executor, from initial family discussions to closing the probate estate, with a focus on Nashville, Tennessee.

Understanding Your Role as Executor

As an executor, your primary responsibility is to ensure that the deceased’s estate is managed and distributed according to their wishes as outlined in their will. This involves gathering assets, paying debts, and distributing the remaining estate to beneficiaries. It’s essential to approach this role with a clear understanding of the legal and financial responsibilities involved. Start by reviewing the will thoroughly to understand its directions and any potential complexities.

Communicating with Family Members

Before proceeding with any legal steps, it’s usually a good idea to communicate with family members and other beneficiaries. Discuss your role and ensure that everyone involved understands the process. This is also an opportunity to identify any potential disputes or misunderstandings. I once worked with a person whose mother had nominated two adult children to serve as co-executors in her will. The parent knew that the children did not get along, but was hoping that they would be able to work together through probate. As you can imagine, this did not go over well. In the event that your family is in disagreement over who should serve, it may be beneficial to discuss alternatives with a probate attorney before speaking with your family.

Finding a Probate Attorney

Navigating probate law can be complex, especially if you are unfamiliar with the legal system. Hiring a knowledgeable probate attorney in Nashville, Tennessee, can be invaluable. Look for an attorney with experience in estate planning and probate, someone who communicates clearly and understands the specifics of Tennessee law. A good attorney will guide you through the process, help you complete necessary paperwork, and represent you in court if needed. Hiring an experienced attorney will save you time and money when it comes to knowing how to proceed with probate.

Handling Court Paperwork and Letters Testamentary

One of the first legal steps as an executor is to file the will with the probate court clerk and obtain letters testamentary. These documents officially recognize you as the executor and grant you the authority to manage the estate. The Tennessee probate process involves submitting the will, the death certificate, and other required forms to the court. Some Tennessee probate courts require a hearing in front of the Judge to open a probate estate and others do not. Your attorney can assist with these filings and any court appearances to ensure accuracy and compliance with Tennessee probate law.

Gathering and Managing Assets

Once you have been granted letters testamentary, your next task is to gather the deceased’s assets. This includes accessing bank accounts, selling vehicles, and managing any other personal property. Keep detailed records of all assets and transactions, as you will need to provide an accounting to the court and/or the beneficiaries.

Your attorney will help you know what assets are in the probate estate and what passes outside of probate. In most cases, anything with a beneficiary designation or joint owner – like a life insurance policy or retirement account- is a non-probate asset. Real estate, such as the home, is typically not part of the probate estate unless specifically mentioned in the will.

Managing Debts and Expenses

As executor, you are responsible for settling the deceased’s debts and expenses. This includes paying funeral costs, storage or mailing fees, attorney fees, court costs, and any valid bills. It’s important to prioritize these payments and ensure that all debts are settled before distributing the estate to beneficiaries. Collecting the deceased’s mail can help you identify any outstanding bills or subscriptions that need to be addressed.

Keep in mind that you are not required to pay debts out of your own money in most Tennessee cases. Your probate attorney will help you determine which expenses should be paid out of the estate and how to handle any bills sent by creditors.

Handling Taxes

Another critical aspect of managing an estate is handling taxes. You will need to file the deceased’s final income tax return and ensure that any taxes owed are paid. While most estates do not owe federal estate taxes, it’s essential to verify this based on the estate’s value and current tax laws. Consulting with a tax professional can provide clarity and ensure compliance with tax obligations.

Distributing the Estate to Beneficiaries

Once all debts and taxes have been settled, you can distribute the remaining estate to the beneficiaries as directed by the will. This step requires careful documentation and communication with all parties involved. Ensure that each beneficiary receives their entitled share and keep records of these distributions for court reporting purposes.

Closing the Probate Estate

The final step in your role as executor is to work with your attorney to close the probate estate. This often involves submitting a final accounting to the court, detailing all transactions, including costs and beneficiary distributions. Ultimately, you should have an estate account balance with zero dollars. Once the court approves this accounting or the beneficiaries waive the filing of an accounting, you can formally close the estate, completing your duties as executor.

Need guidance on managing a loved one’s estate? Schedule a free initial call with our team at Graceful Aging Legal Services to discuss your specific needs and how we can assist you through the probate process.

Serving as an executor is a significant responsibility that requires organization, communication, and attention to detail. By understanding your role, seeking professional guidance, and following the legal steps outlined in this guide, you can honor your loved one’s wishes and navigate the probate process with confidence. Remember, you are not alone—resources and support are available to help you through this journey.

Last week we looked at red flags you should pay attention to with regards to caregivers and professionals in your network. This week we’ll look at how to prevent abusive caregiver situations and how to deal with abuse once it has occurred. Below are some actions you can take to guard against people in your network taking advantage of you.

Things you can do now:

Take advantage of your free yearly credit report.

You can get a free credit report from each of the three credit reporting agencies (Experian, TransUnion and Equifax). Hot tip! Space them out! Sign up to get one every four months. This will make it easier to discover any irregular activity fairly quickly.

Ask your banker if they have completed the “BankSafe” program from AARP.

BankSafe is a training platform designed to help financial professionals identify and stop suspected exploitations from caregivers. Ask your bank if they have participated in this training. If your bank has not had this training, encourage them to do so! Or consider moving funds to a bank or credit union that has already participated.

Budget for paid assistance.

Remember that as much as family and friends may want to help, sometimes they can’t. It’s important to make sure that you are able to afford assistance for things like traveling to appointments, grocery shopping, laundry, nutritious meals, cleaning, and other personal help you may need if you were injured or developed a medical condition. Endeavor to have enough of your retirement savings to ensure you can afford a positive work environment for your future caregivers.

Create a Durable Power of Attorney

Create a Durable Power of Attorney.

This Power of Attorney allows someone you trust to monitor and manage your finances, if needed. This could be a family member or close friend. With access to bank accounts and credit card statements, they should be able to notice quickly if your spending habits change or if there is fraudulent activity on your account and they’ll be able to file a claim to protect your money!

Things to keep in mind for later:

Listen to your loved ones.

If you have a caregiver that is not in your family, do yourself a favor and trust a loved one’s opinion if they sense unsettling behavior from that caregiver. Sometimes others are able to see things that we are too close to observe.

Don’t become too reliant on one person.

You can have a housekeeper come every other week to clean the surfaces, a home health nurse to check on your health, and a food delivery service to prepare your meals or deliver groceries. Surround yourself with people who like their jobs.

Let family and friends know you welcome their visits and calls.

Tell them what has been going on in your life and find out what is going on with them. Maybe a few favorite snacks in the cupboard will even bring the grandkids by.

Let family and friends know you welcome their visits

Don’t give up your routines.

Self-care is so important, we all know that! If you feel yourself falling into a slump, get outdoors, go to the store, call a friend or ask someone for help. You deserve to be loved and to love yourself. No matter what anyone says, you are the conductor of your life.

“Stranger danger” isn’t just for children.

As adults we get comfortable interacting with all kinds of people, but remember that not everyone has your best interest in mind. Beware of helpful people who appear out of nowhere! Trust your instincts and listen to your inner-voice.

Don’t keep secrets.

If anyone tells you to keep a secret from your friends or family, something is very wrong. Red alert!

Report anyone who threatens to physically harm you.

Call the police and tell your trusted loved ones. There are no second chances when it comes to your personal safety.

Practice being assertive with others

Remember that “no” is a complete sentence.

If you are a people pleaser, practice different ways of saying “no” so you’ll be more comfortable in situations where you need to say it.

This week we are going to talk about why you need a medical power of attorney, even if your spouse is available to make decisions for you.

In a medical emergency, there is an assumption that your spouse would be the health care agent, make health care decisions, and deal with the hospital and doctors on your behalf. However, what happens when a spouse is separated, no longer wants to be in contact, or doesn’t agree with your health care values?

If this happened to you, would you still want them to make decisions for you? Do you want your adult children to make medical decisions for you? What if your spouse and children disagree on what type of treatment(s) you should receive? When faced with an emergency, please consider having your medical Power of Attorney already in place.

What happens if you don’t have a Medical Power of Attorney?

There are many situations that can arise when you become incapacitated or have a healthcare emergency. Even if it seems unlikely that your spouse would be disinterested in your health, it’s important to remember that your spouse may have trouble thinking clearly in an emergency or may also be seeking medical care. A medical Power of Attorney with an agent that is capable of making medical decisions, even in an emergency, can lower the risk and confusion regarding your medical decisions.

What is a Medical Power of Attorney and why you need one.

A medical Power of Attorney, also known as a Durable Power of Attorney for Healthcare, is a document that allows you to appoint someone as an “agent” to make decisions about your health care. This agent will make decisions on your behalf if you become too ill or incapacitated. A medical Power of Attorney ensures that your wishes will be followed. We have an experienced estate planning and probate attorney here in Nashville who can help you customize these decisions and record how choices will be made.

Choose someone you trust to make medical decisions for you.

How to choose the best Agent for your situation

When you are choosing your medical agent for your Medical Power of Attorney, it is important that you choose someone you can trust to adhere to your preferences regarding your medical care. Discuss your wishes with your agent before they need to make any care decisions. Make sure that you have confidence that your Agent will make the right decisions about things you two have not discussed.

Don’t wait to create your medical POA.

Conclusion: Why everyone needs a Medical Power of Attorney

It is important to think about what you would want in a medical emergency. Do you want your spouse to always make decisions for you?

Designate ONE person authorized to make decisions for you if you are unable to make or communicate your wishes. Even if you want your spouse to make those decisions, it’s always a good idea to have a “backup” person. This backup person can help out with decision-making in case your spouse is unavailable when someone needs to step in.

Whatever you decide, you should have a Medical Power of Attorney. Write your power of attorney in conjunction with your advanced directive (also known as a living will). All of these documents are an important part of a well-thought-out estate plan.

Do you have a plan for emergencies? Do you want help putting your values on paper? Take our Virtual Estate Planning Challenge! This 7-part Challenge helps you brainstorm the important stuff before creating your estate plan. We had a ton of fun making it and think you’ll really benefit from it too.

Last week we defined TennCare and how it applies to our clients. This week I want to go more in-depth with how TennCare serves Tennesseans with long-term care.

Many people believe that Medicare benefits will cover nursing home care once an individual is 65 or older, but this simply isn’t true. While Medicare covers the first 100 days, it doesn’t cover long-term assisted living. Read more about Medicare here.

“ Choices” is Tennessee’s Medicaid program for long-term care services and support

Back to TennCare/Medicaid…

My Mom doesn’t have long-term healthcare insurance. What are my options?

Payout of pocket until you run out of cash – This is an unrealistic option for most families. Nursing home care is expensive. Not a lot of people have an extra $7,000-$11,000 a month in their bank accounts.

Do a reverse mortgage on her home.

Qualify for the TennCare / Medicaid program called “CHOICES”.

As you can see, options 1 and 2 are very unpleasant and leave nothing left for a loved one’s legacy. However, option 3, CHOICES, is definitely something worth looking into.

What is CHOICES?

CHOICES is the category of TennCare that provides Long-Term Services and Supports (LTSS) such as nursing home care.

What is the process for getting qualified for CHOICES?

In order to be eligible to receive benefits from TennCare/Medicaid your loved one must first qualify within these three categories:

Medical eligibility

Income threshold

Asset threshold

Being medically and financially eligible is necessary for TennCare approval

How does someone become medically eligible for TennCare CHOICES?

The state of Tennessee will determine who is medically eligible to receive TennCare Long-Term Services and Support (LTSS) by using a pre-admission evaluation (PAE). This PAE is used to determine if the applicant can do basic life skills on their own without help. The PAE will also determine if the applicant is safe in their current environment.

The PAE is a strict evaluation and it is performed on a case-by-case basis. An applicant must receive a score of 9 or higher on a 26 point scale in order to be considered medically eligible for TennCare Long-Term Support Services.

For example, a caregiver or healthcare provider may be asked about a patient’s level of ability to do things and how much assistance is needed.

The following Activities of Daily Living (ADLs) are covered in the PAE evaluation:

Transfering

Mobility

Communication

Medication

Orientation

Eating

Behavior

If you or your loved one is unlikely to get to a nine or higher on the PAE, it is always appropriate to ask for a “safety determination” evaluation as an alternative route of becoming medically eligible for Choices.

How can someone become financially eligible to receive CHOICES?

You must be able to prove that the applicant has a low income and little assets. As of January 2022, an individual applying for TennCare CHOICES cannot have an income exceeding $2,523.00 per month. Additionally, the applicant cannot have more than $2,000 in assets. This includes any money in the bank and investment accounts but also requires consideration of retirement accounts, life insurance policies, real estate, artwork, jewelry, and any other valuables. When we talk about the assets for a couple of things get a little more complex. The most important thing is that both the applicant and their family are taken care of, both medically and financially.

My Mom is over the limits for income and assets? What do we do?

If the applicant is in excess of the amounts we can plan for that! We have a tool to help people who have excess income and assets yet need to qualify for TennCare/Medicaid called the “Care and Savings Assessment”. With this Care and Savings Assessment, we work to determine the best way to structure you or your loved one’s finances, either now or in the future. We plan so that our clients have the peace of mind knowing they can qualify for TennCare if and when they need it!

In conclusion

It is often helpful to have an attorney assess your financial situation and offer recommendations on how those finances may be restructured to qualify for TennCare Long-Term Services and Support (LTSS). As an experienced TennCare planning attorney, I can help you evaluate your risk and create a plan that takes care of everyone in the family.

Are you ready for help with TennCare planning? Contact us and we can discuss your plan. Next week we will go over some examples of how we restructure an individual’s finances to meet their needs for long-term care.

This month we will discuss the subject of powers of attorney. In week one, we will discuss how to name a financial power of attorney. This is also known as a durable power of attorney.

There are many things to consider when appointing a financial power of attorney (aka an attorney-in-fact). This is an important position. Whoever you appoint would have the ability to make decisions regarding how you manage your finances. While it may seem obvious, it’s important to focus on choosing someone who is organized, trustworthy, and financially responsible.

What powers does an agent have when they have a financial power of attorney?

As stated earlier, the agent with a financial power of attorney can handle your finances just as you can. An agent will have the ability to go to your bank and handle banking transactions. They can contact your investment account broker and manage those funds. They can handle your insurance and sell your house. Of course, you want your agent to only make financial transactions in your best interest while you are incapacitated.

Can things go horribly wrong? Yes! Your agent has the power to clean out all of your bank accounts and sell your home. Heck, if they wanted to, they could take your assets, move to Fiji, and set up a little beach bar! I want to reiterate: It’s important that you choose someone who would never even think of doing something like that. You need to choose someone who will only have your best interest at heart.

Who should be your financial power of attorney?

When considering who should serve as a financial power of attorney, a lot of people are compelled to choose someone close to them. A lot of times this will be a relative, such as your children or possibly a sibling, but it doesn’t have to be. The agent could also be a close friend or even a professional if that is who fits that role in your life. In our practice, we like to make sure that our client acknowledges this very important point: the person you name as your agent in a financial power of attorney will have the ability to handle your finances pretty much the same as you will.

Choose an agent who can communicate effectively

Not only do you need to trust your agent, but we also recommend that you find someone that other people trust! While this element is not completely necessary, it may be important to you that your agent be relied upon to communicate important information effectively with the people in your life.

For example, if one of your relatives says to your agent: “Hey, my Aunty saved a lot of money and invested it well, how much does she have now and what has the spent money been used for?”. Ideally, you would have an agent that relatives intuitively trust to spend your funds in your interest. However, it would be really awesome if your agent took the time out of their day to respond thoroughly to your relative’s questions.

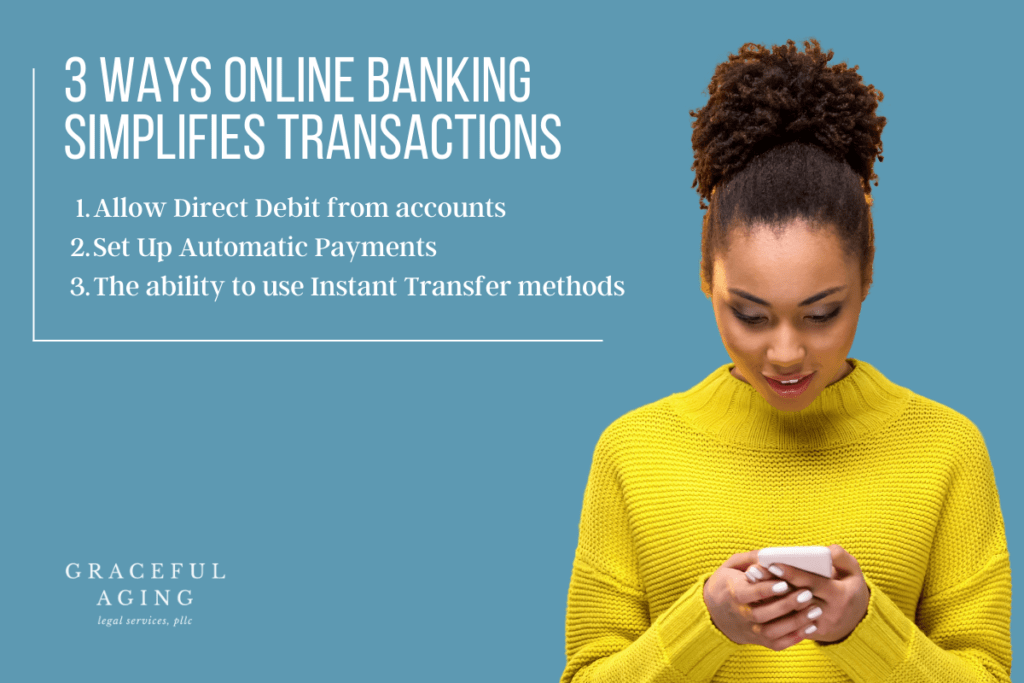

Choose an agent that is comfortable with online banking

Your agent should be good at bookkeeping

In a perfect world, your agent with financial powers of attorney would be held accountable for the transactions coming out of your assets. A good agent can effectively answer questions about spending and back it up with good bookkeeping!

An agent with power of attorney does not have to live in your state

As we mentioned before, the era of digital banking is here and it allows us the option to choose from a larger pool of agents, regardless of their location. Now, many people think that their agent under a power of attorney cannot be someone who lives out of state. And that is simply not true. Sometimes it helps to have somebody who lives in the state, but that is not a requirement in Tennessee. We do so many things by email and telephone, texting, and online business transactions that your financial power of attorney person, your agent, will likely be handling any business transactions online.

Choose an agent who will outlive you

While this is not a requirement, it is a good idea to think about someone who will outlive you. Generally, when you are using your power of attorney, it’s when you’re incapacitated. While there are times when a durable power of attorney is used on a temporary basis, such as during a medical event, it is more likely going to be during a period when we are at the end of our lives and are experiencing some type of ongoing health condition that is not likely to improve. We recommend that you look for an agent who can help on a continuing basis. A well-suited agent allows everyone to relax and enjoy the time you have left on this earth.

Who should NOT be your durable power of attorney

Again, while it may seem obvious, it is important to reiterate that anyone who is untrustworthy, unlikeable, terrible with money, incapable of balancing a checkbook, or unable to effectively use online banking might not be the best choice for becoming an agent of financial power of attorney. The goal is to find someone who can keep good accounting records and knows exactly where your money went, down to every last penny! A good agent is someone who is willing to communicate with everyone without hesitation. The main point is that no one in your circle should be concerned that your agent is taking advantage of you if you are incapacitated.

Now, if you are not incapacitated, your agent should only be acting if you are telling them to do so. Even if you have your power of attorney take effect immediately, your agent can and should only act under your direction. If you find that the agent acts otherwise, there are legal actions you can take against them in court.

In conclusion

A power of attorney is a useful tool for organizing the “adulting” part of your life, especially in incapacitation. A financial power of attorney should be someone that you absolutely trust; someone who will not give pause to others in your life. Someone who is financially responsible and organized, and someone who is familiar with handling online transactions. It does not matter if your agent lives in your state. In short, find an agent you believe will always have your best interest at heart.

There are many types of powers of attorney. Many powers of attorney are used when creating a well-thought-out estate plan. Do you think you could use a durable power of attorney in Nashville? Schedule an initial call to see if we can help you with your situation.