Quite simply, TennCare is Tennessee’s Medicaid program. While the name “TennCare” has the word “care” in it, it is NOT Medicare. In order to further clarify the difference between the terms “Medicaid” and “Medicare,” you need to remember that we use “Medicare” to “care” for our elders and “Medicaid” to “aid” those, of any age, in need. Essentially TennCare is Tennessee’s brand of Medicaid. Hopefully, that little trick will help you remember the differences between each program.

Who qualifies for TennCare?

Now that you are familiar with the difference between Medicare and Medicaid, let’s discuss who qualifies for TennCare (Medicaid).

There are three qualification criteria that you must meet in order to obtain Medicaid/TennCare.

1. Medical qualification –There is a special medical test that applicants must pass in order to qualify. Usually, a care facility will handle this piece of the Medicaid application.

2. Asset qualification – A TennCare applicant who is single can only have $2,000.00 in assets before they are eligible for TennCare. Vehicles and real estate are usually exempt from the count of assets. A “Care and Savings Assessment” is a good place to start if the applicant needs help with figuring out what they have in assets and what options are available to make excess assets “non-countable” for TennCare purposes.

3. Income qualification – A TennCare applicant can only receive $2,382.00 per month (as of 2021) in order to receive TennCare. If an applicant has more than this amount in income, an attorney can resolve it through what is called a Miller Trust or a Qualified Income Trust.

Long-term care is very expensive

Why should I be concerned about long-term care services?

Unless you are a millionaire or multi-millionaire, TennCare eligibility and designation could have a major impact on your finances and your family. While you may not need TennCare now, you will want to plan as if you will need it in the future. As you may have heard us say before “we hope for the best, and plan for the worst.” Having a plan is an effective way to ensure that you will have long-term care coverage when you need it. This isn’t to say that you won’t find yourself needing TennCare much sooner than expected. When this happens we call it “TennCare Crisis Planning”.

Knowing your options makes all the difference

I don’t know where to start!

The biggest obstacle to TennCare planning is determining what to do with your assets and income; especially if there is excess in any category. There are a lot of rules and potential pitfalls that you need to look out for. Fortunately, we have some great financial planning and legal resources that can help our clients. If you have an immediate need for TennCare or want to plan for TennCare we can supply the client with what we call a “Care and Savings Assessment”. It’s a wonderful tool that helps people effectively navigate through their options.

How do we help our estate planning clients with TennCare planning?

For our estate planning clients, we like to take into consideration the possibility that you may need TennCare in the future.

For example, it is our priority to set up our client estate plans to make sure that TennCare is accessible if it is ever needed. As with many government organizations, Medicaid has lots of rules to follow and many people find that they did not know what rules they were supposed to be following until it was too late! Fortunately for our clients, we know the rules and can help you plan in advance of ever needing to apply for TennCare to cover medical care. Additionally, we create documents that make sure that someone can apply for Tenncare on your behalf. This is useful if you become incapacitated in the future.

How do we help our Conservatorship clients with TennCare?

Many of our conservatorship clients are caregivers for a loved one who requires skilled nursing to keep them safe. The average cost for this type of care is about $7,000.00 per month or more. There is usually a large gap between monthly income and fees. Our firm can navigate the TennCare application process and assure that the appropriate language is in the conservatorship order paperwork with the court so that the client may obtain the appropriate benefits for their loved one.

How do we help clients with TennCare Crisis planning?

For those who have never considered the cost of long-term care until they or a loved one need to enter a nursing facility, the cost of care is likely to come as a shock- and an unaffordable, but necessary, expense. This is when we can step in with what we call “crisis planning,” meaning that you need a plan and you need a plan now.

In these cases, we are able to look at the household financial situation of the person needing skilled care, as well as the family situation overall, and come up with a plan for how to best use existing resources and get them qualified for TennCare benefits to pay for the nursing home bills. This process called our “Care and Savings Assessment”, is one of the most rewarding things that we do! It allows us to help people get the care that they need while still providing a quality of life for themselves and their families.

If you are concerned about accessing TennCare benefits for long-term care, contact our office for a complimentary initial call using our online calendar here.

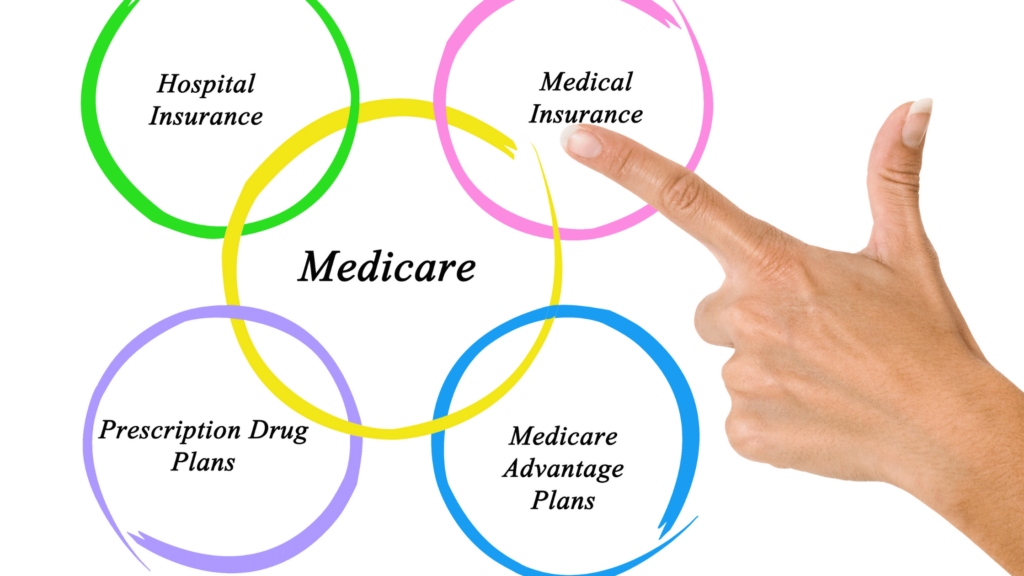

As if choosing health insurance under an employer’s plan wasn’t difficult enough, figuring out which type of Medicare plan is best for you is even more confusing. I call Medicare an alphabet because there are 4 parts- A, B, C, and D. Oh, and you might want to consider a supplement too!

Don’t worry. With a little time and some guidance, you can master the Medicare alphabet just like you mastered your ABCs!

First, let’s go through the four types and what they cover.

Part A only covers emergency care, such as if you need to stay at the hospital.

Part B covers regular care like doctors visits, bloodwork, and any other testing or treatment that your doctor recommends.

Part C is often referred to as an “Advantage Plan”. It is administered by private insurance companies, just like an employer’s plan. It includes Part A and B coverage and may include other benefits as well, such as dental, vision, and prescription drugs.

Part D covers prescription drugs. That’s it.

When you approach age 65, ask yourself what your current health needs are, what family history might impact future healthcare needs, and what type of coverage you are used to receiving. Then look at your budget.

Part A is free for those who are eligible through their tax contributions. In 2021, most individuals will pay $148.50 per month for Part B, although the amount can be higher depending on your income.

If you anticipate that you will need something more than just emergency and regular doctor’s visits, there is another alternative. Consider a Part C “Advantage” plan or a Medicare Supplement (or “Medigap” plan), instead. This plan will provide coverage for those things that Parts A and B don’t, like such as prescription medications, dental, or vision care. Keep in mind that you still pay co-pays and deductibles on Medicare, so you will want to look at those amounts and not just your premium when considering your budget.

When thinking about the Medicare alphabet, I have a little way to help me remember what each part covers:

A is for an Accident that lands you in the hospital

B is for Bloodwork they do at the doctor’s office

C is for Comprehensive coverage you can get with an Advantage plan

D is for Drugs (They made that one easy!)

Now you know your ABCs….next week I hope you’ll join us when I share my favorite FREE resources to learn about Medicare before you sign up.

Choosing a legal guardian who can raise your kids if you are unexpectedly incapacitated or pass away can be a daunting and difficult challenge. There are many things to take into account such as parenting styles and the potential guardian’s ability to love and take care of your children.

These are just some of the questions we believe every parent should answer before naming a guardian.

Where will your children live? Many parents desire to keep their children in a familiar environment if something unfortunate happens. It’s not unusual for parents to put instructions in their estate plans regarding the cities or states they want their kids to be raised in if mom or dad passes away. If the geographical location of where your kids will be placed is important to you, be sure to make this known to your Davidson County will attorney when creating your plan.

Are your children familiar with the potential guardian? It is important that your children are comfortable with the guardian you are about to choose for them. If you are selecting a guardian that lives far away, you may want to consider ways to begin cultivating a relationship between your children and the potential guardian before it’s needed. Naming a temporary guardian is also important in such situations. This will ideally be a person that lives close by and can help ease the transition to your kids relocating to their permanent guardian’s home.

Is your potential guardian prepared to care for your children? There are many factors that could fall under this category, but it is important to make sure that your guardian is emotionally, physically, and financially prepared to care for your child/ren. For example, you may want a grandparent to become guardian, but their age and their own financial and/or medical needs may make serving in this role difficult for them. Don’t forget to take their point of view into account when making your selection.

Do any of your children need special care? If you have a child with a mental or physical disability, it could take special knowledge and resources to care for your child. It is important to make sure that the named guardian would not be overwhelmed by this responsibility and that they are prepared to care for your child in whatever way that your child may need.

Have you discussed this choice with your potential guardian? It is very important that you ask your potential guardian if this is a responsibility that they can take on. You will also want to talk about your desired path for raising your child/ren to make sure that you are in agreement and that your wishes will be followed.

As parents, you spend a lot of time planning the best future for your children. Make sure that your planning includes naming a legal guardian should you become unexpectedly incapacitated or pass away. You should be the one making that decision – not the courts. Schedule a call with our Davidson County will law firm today, so you can have the peace of mind knowing your children will be cared for by the person you want, in the way you want if anything happens to you.

From a legal standpoint, parents don’t have a lot of rights after you turn eighteen. But we often rely on our families more than we realize, something I was jerked into remembering during my junior year of college when I was rushed to the emergency room and soon told that the surgical team was ready for me. Ummmm….can’t I call my mom first???!!!

Fortunately my situation worked out, but as a lawyer, I can’t help thinking about what if I had not been awake to call my parents. What if I needed more extreme medical treatment and couldn’t tell the doctors what I wanted?

Here’s what you need…

This is where you can learn from my mistakes. Get your legal shit together before you head off to college. Or after. But as soon as you can. I will even help you get everything completed by video call.

As a bona fide adult, you need a minimum of three documents in case of an emergency:

Healthcare Power of Attorney– This document allows you to appoint someone you trust to make decisions if you can’t communicate with your medical providers.

Financial Power of Attorney– A financial power of attorney allows you to give someone else permission to act on your behalf on financial matters. That means paying bills, completing financial aid or loan applications, dealing with insurance companies, and other ways that, well, adulting sucks. You’ll need to choose whether you want this to become effective immediately or only when you are unable to handle your own business.

Signed HIPAA Form– Now that your parents don’t have access to your medical records, you might want to consider authorizing someone to see them. Often family is a good go-to for all things medical (see: hereditary conditions) but you can name anyone-and everyone- you’d like. Mom, Dad, Brother, Best Friend, Fifth Grade Teacher? If you love them enough to share your blood panel results, then a HIPAA waiver is no biggie.

If you wanna get fancy, you can also sign a FERPA waiver to let your trusted adult have access to your educational record. It’s the grown up version of the school sending home your report card to show how smart you are. 🤓

Who should you name?

These are your documents, so you can name any adult you want to act in case you can’t (or don’t want to). In most cases that’s a parent, but let’s be real. Not all parents are created equal. Sometimes your “trusted adult” is your aunt, your neighbor, or your cousin. Whoever you name, it should be someone you trust with your life and your 💵 bank account.

When you’re ready to start getting your adult shit together, just text the word ADULTING to 615-846-6201. The cost for all of these documents together is $500 through our office. Your family might even be willing to foot the bill if you show them how responsible you’re being!

In life, there are jobs we seek out and others that are given to us. Being named an Executor (or Personal Representative) of an estate is one of the most important jobs one can be asked to hold by another person. It means there is someone who trusts you fully and believes that you will manage their final wishes properly and without conflict.

That’s not to say the job is easy. Again, you were likely appointed to the role of Executor because your loved one felt you could handle any stress or difficult responsibilities that come with the job.

The good news, however, is that there are ways to prepare in advance so that your life as an Executor is easier when the time comes. Here are some suggestions a Middle Tennessee will lawyer would have you consider:

Have the hard conversations now. Meet with the person who is naming you as an executor of their estate and ask them to describe exactly how they wish their estate to be administered. Take notes and make sure you get all the details. Knowing the “why” behind the decisions in the will can help you navigate “gray area” choices if they arise.

Be organized. The job of an Executor consists of lots of paperwork, bureaucracy, and time maintaining the estate as it goes through the probate process. Set up a filing system, spreadsheets, and bins, so the Executor’s job does not infringe on your everyday life.

Get a lawyer. No matter the size of the estate, it is prudent for all involved parties to have a lawyer. At the minimum, have a consultation with an attorney to make sure there is not something you have overlooked. People often think they can do everything themselves only to be caught at the end by taxes or administrative issues.

Move quickly once the person passes away. Grief makes people act in unexpected ways, so it is imperative that after the person dies, you move quickly to locate the original final will and file the necessary paperwork with the courts to be recognized as the Executor. At this time, order up to 8-10 copies of the death certificate to save yourself time later. Another uncomfortable thing you will need to do is to secure the assets. All too often, grieving loved ones will go to the home and begin to take items they believe they should have. You will have to be the one who stops this.

Be upfront with the heirs of the estate. Make sure they all get a clear understanding of how estate administration works. The process is a slow one, which frequently frustrates family members who are grieving. By giving them an explanation or better yet, having a lawyer do it, they will hopefully have patience with you and avoid conflicts.

Know there will be conflicts. Grieving is an individual process, and you will take the brunt of most of that emotion. If money is involved in the administration, the speed at which money is inherited can be infuriating. Heirs becoming angry with you is even more of a probability if any perceived omissions or secret bombshells are in the will. Hopefully, if that is the case, you knew ahead of time and were prepared.

Heirloom distribution needs to be deliberate. Once the significant assets and personal items are named in the will, the hard part starts. Deciding who receives the personal items in the home can cause the most conflicts. There is no explanation for the small household items that might have importance to many family members. A sweatshirt, a picture frame, or a dish can hold deep memories that you might be unaware of. Creating an equitable system for if multiple people want an item will ensure this process is done deliberately.

These are only a few ways you can help yourself if you have been named an Executor. If you find yourself struggling with your duties or you have questions and need some advice, we are here to help. To have an appointment with our Middle Tennessee will lawyer, April, schedule an initial call with us today!